Why Today’s Inflation Is More Dangerous Than the 1970s

In this week's "Deep Dive", we dig into the weeds of today's inflation and its striking resemblance to the 1970s breakout. But make no mistake, this comparison isn't as straightforward as many think.

The 1970s is the ultimate American allegory of inflation.

By official measures, it was the worst inflation rout in America’s post-war history, with inflation peaking at 14.6%. It was also a bitter lesson about what happens when policymakers bide their time—for political gain and whatnot.

So, naturally, the 1970s is always the reference for the worst—like that naughty kid in school that parents benchmark their own kids against. That comparison is especially tempting this time around.

Just like today, the 1970s inflation was a by-product of both extra loose monetary policy (demand-pull inflation) and energy shocks (cost-push inflation). It is, therefore, probably the best reference there is to predict what’s to come.

The catch: it’s not as straightforward as many make it out to be.

Loose monetary policy

In 1971, Nixon de-pegged the dollar from gold and turned it into the free-floating fiat currency as we know it today. And because the dollar was no longer backed by gold reserves, it freed up the Fed’s hands to pump dollars into the economy.

Two years ahead of Nixon’s reelection, the Fed, allegedly pushed by the Nixon administration, launched an aggressive expansionary monetary policy despite concerns over growing inflation.

Then-Fed chair Arthur Burns slashed rates from 9.5% to 3% and grew the M2 money supply on average 12% year-over-year until after Nixon’s reelection.

(For perspective, the world hasn’t seen as high y-o-y growth in M2 money supply until Covid.)

Then Burns compelled Nixon to implement wage and price controls because he believed (or pretended to) that surging inflation had nothing to do with his policy. Instead, he blamed labor unions and big corp for stoking inflation with higher wages.

Price controls did help tame inflation temporarily, and at the expense of nationwide shortages. But in the long run, it was like a Band-Aid on a gunshot wound. It masked the symptom but didn’t solve the underlying problem.

So after the price lid was lifted in 1973, businesses just raised their prices to make up for lost ground, and the pent-up inflation blasted through the roof.

Oil shocks during the 1970s

Then there was a substantial cost-push element.

In 1973, OPEC, which at that time pumped seven out of 10 global oil barrels, banned all oil exports to the U.S. and its allies. It was retaliation against the West for supporting Israel in the Arab-Israeli war.

The first oil shock started.

Back then, the U.S. didn't have strategic national reserves. And addicted to cheap Arab oil, it had cut its domestic production down to a minimum. From WWII to 1971, the U.S.’s share of global oil production dropped from 64% to 22%.

So, by 1974, deprived of Arab oil, the U.S. began facing oil shortages and oil prices quadrupled from $3 to nearly $12 per barrel.

Then the Iranian Revolution happened.

Although its disruptions led to just a 7% drop in global oil production, the fear of the unknown set off a blaze of speculation. The second oil shock followed and by 1980 crude oil prices ballooned to $39.

(In today’s dollars, price increases during both oil shocks would be equivalent to crude oil going from $24 to $142 per barrel.)

Post-Covid inflation drivers

Fast forward to February 2020.

The Covid pandemic sweeps the world. The Fed immediately steps in by slashing rates to zero and injecting an unthinkable $4.8 trillion in the form of quantitative easing (QE). That alone amounts to more than the U.S. spent during WWII.

But unlike in 2008, this time around QE was combined with massive fiscal spending, including direct money transfer through stimulus checks (or in monetary terms: helicopter money).

As part of Covid relief spending packages, Congress handed out nearly $5 trillion. This isn’t some QE that ends up in bank reserves. That’s a direct money injection into the economy, which works like gasoline onto a fizzled-out fire.

In all, by mid-2021, the U.S. had spent $13 trillion on Covid, which is more than it spent during all its 13 wars, combined.

Ray Dalio dubbed this policy approach “Monetary Policy 3” (MP3). And slamming Powell’s “transitory inflation” narrative, Bridgewater was one of the first asset managers to call inflation a policy error rather than a Covid supply shock.

From Bridgewater (emphasis mine):

This is not, by and large, a pandemic-related supply problem: as we’ll show, supply of almost everything is at all-time highs. Rather, this is mostly an MP3-driven upward demand shock. And while some drivers of higher inflation have been transitory, we see the underlying demand/supply imbalance getting worse, not better.

The mechanics of combined monetary and fiscal stimulus are inherently inflationary: MP3 creates demand without creating any supply. The MP3 response we saw in response to the pandemic more than made up for the incomes lost to widespread shutdowns without making up for the supply that those incomes had been producing.

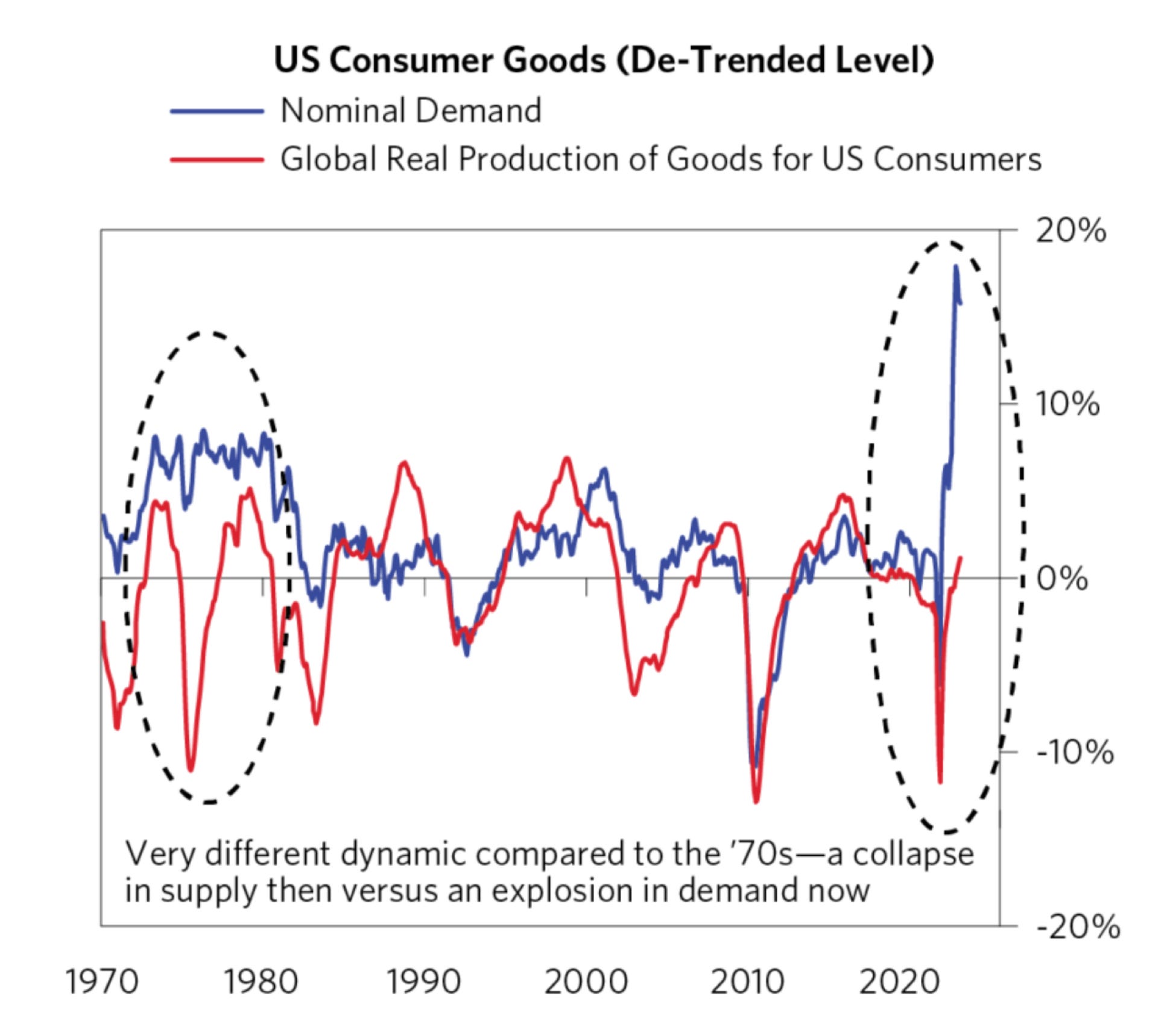

The stimulative effect of a mixture of unprecedented monetary and fiscal stimulus is clearly seen in the historic uptick in demand for US consumer goods.

And as of last December, the mismatch between demand and supply closely resembled the divergence during the 1970s inflation breakout:

Then, once again, history rhymed with the 1970s.

In February 2022, Putin shocked the world by mounting an all-out invasion of Ukraine and starting the biggest war (ahem, “special military operation”) in Europe since WWII.

In response, the West slapped a barrage of sanctions on Russia, including window-dressing oil bans, which didn’t mean much, especially for the U.S. Russians retaliated. Putin expanded the West's selective embargo (banning things that give the impression of action, but don’t wreak havoc on their economy) to things that really hurt Western powers.

For starters, Russia’s army seized all Ukrainian ports along the Black Sea and blocked millions of tons of food exports from Ukraine. That’s a big deal. Ukraine is the EU’s fourth-largest supply of food and one of the world’s largest producers of staple grains.

The Kremlin also leveraged its position as the world's biggest fertilizer producer and imposed strict quotas on its exports. And while the United Nations mediated a “grain deal” in July to restart grain and fertilizer exports, recent UN reports show that Russian exports haven’t recovered.

Fertilizers are one of the key inputs in food production. And without Russia, the world can't source enough of them—which is devastating yields, urging some food producers to shut down their operations, and, in turn, further stoking food prices.

And last in the saga is Nord Stream.

Since June, Russia has been tapering its gas flows to Europe through Nord Stream and disguising its actions using “maintenance” and all sorts of other bogus excuses.

And last month, before the mysterious Nord Stream explosions, Russia shut down the pipe completely, threatening that it wouldn’t put it back online unless the West lifted its sanctions.

From an economic and geopolitical standpoint, Nord Stream’s shutdown is Europe’s version of OPEC’s oil embargo. Europe generates around one-third of its energy from gas, and most European nations, including its economic powerhouse Germany, source most of it through Nord Stream.

So, after the shut-off, gas prices went through the roof in Europe and across the world.

For perspective, compared to pre-Covid times, European benchmark gas prices peaked at 10x higher prices, and in the U.S. they were at 3x pre-Covid levels before retreating in recent months.

Now here’s another interesting parallel with the 1970s.

Last month, Europe’s largest economies announced they would pass $375 billion in fiscal packages to last through the winter. The UK alone wants to spend $150 billion within the next year and a half.

Relative to the U.S. economy size, that amounts to a $1 trillion package.

All this money will go to cap energy prices for households and businesses for the next year or so. For example, Britain is expected to cap electricity and gas bills for businesses at “half of the expected wholesale prices.”

That’s price controls all over again.

Of course, they are as intrusive as Nixon’s all-encompassing wage and price controls because they cap just energy costs. But on the other hand, energy is one of the key inputs in the production of everything.

So capping energy prices is in a way capping part of the price of every good and service in the economy.

Peak or trough?

With all that’s happened (and still happening), headline CPI in the US isn’t in such a bad place. By a plain comparison, it’s still far below the 14.6% peak of 1980. But does this divergence really explain the extent of today’s inflation?

Last August, CPI rose 8.1% year-over-year and 0.1% compared to a month ago, shredding the “inflation is moderating” narrative to pieces. What is most worrisome is that core CPI—which is stripped of volatile energy and food prices—has risen for the first time in half a year:

The same in the EU.

In September, the EU’s core inflation jumped to a record high of 6.1% with virtually every category showing high readings:

That’s the last nail in the coffin of the “transitory inflation” thesis because this data tells us that exploding energy prices are successfully feeding inflation through the rest of the economy.

Until very recently, energy prices were a matter of utility bills and prices at the pump. Now they are being passed on to final products, from industrial goods to steak and lettuce at the grocery store.

We’ve seen a similar lag in the 1970s.

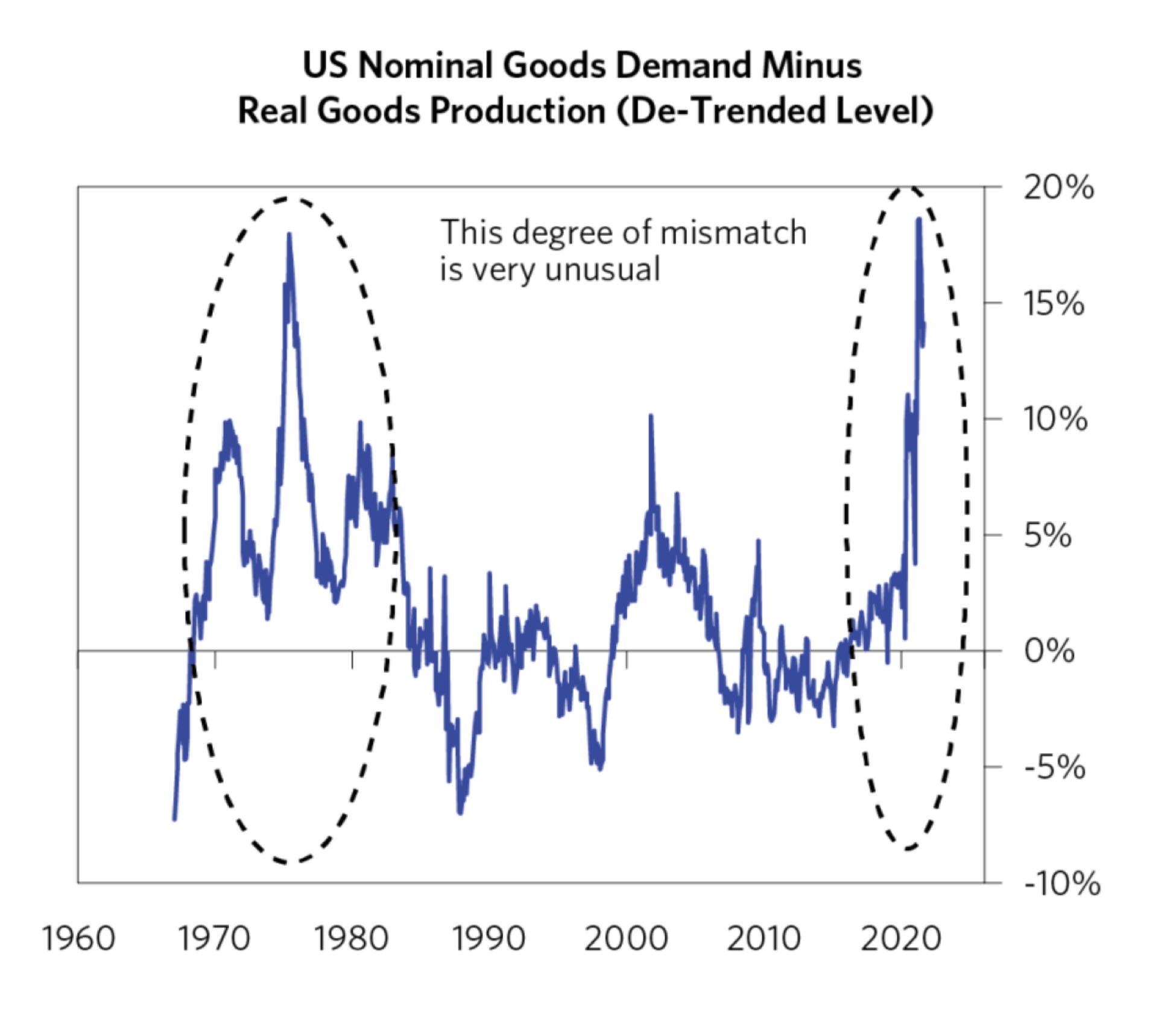

Take a look at this next chart once again. See how inflation lagged behind both the surge in money growth and oil shocks. Back then, inflation peaked only two years after explosions in energy prices:

But even then, comparing those peaks and troughs to today’s CPI is apples to oranges for two reasons.

First, there have been a number of revisions to how CPI is calculated. And by far the most important change was introducing the concept of owner’s rental equivalent (ORE). Here’s a good explanation from Larry Summers:

Housing is both a consumption good and an investment. Between 1953 and 1983, the Bureau of Labor Statistics (BLS) valued homeownership costs for the CPI without disentangling these two qualities. It produced a measure that broadly captures changes in the expenses of homeowners, taking house prices, mortgage interest rates, property taxes and insurance, and maintenance costs as inputs….

In 1983, after ten years of internal debate, the BLS exchanged homeownership costs for owners’ equivalent rent (OER). By estimating what a homeowner would receive for their home on the rental market, the BLS stripped away the investment aspect of housing to isolate owner-occupiers’ consumption of residential services.

The result is that back in the 1970s, shelter inflation largely tracked interest rates because the higher the rates, the higher the mortgage bill, which was the biggest shelter expense that went into pre-1983 CPI:

In the end, it made it seem as if CPI was much less responsive to monetary tightening and higher than it should technically be.

So, to draw a better comparison between today’s CPI and one during the 1970s breakout, Larry Summers with his peers from the IMF and Harvard University, revised the 1970’s CPI to reflect today’s CPI methodology.

Here’s what it looks like:

By this measure, today’s inflation is very, very close to 1980’s peak.

Now, the second change in CPI is that its weights have significantly evolved due to structural changes in the economy. Over the past 50-70 years, American expenditures have largely shifted from goods to services.

For example, as Summers points out, “In the early 1950s, food and apparel accounted for almost 50% of the headline CPI index.” Today these categories get just 17% of the weight in CPI.

The bottom line is that headline inflation today is less driven by volatile “transitory goods” that dominated CPI in the 1970s and more by services that are less volatile, and most worrisome, more sticky.

What we can make of all this

If history is any indication, inflation lags in the 1970s signal that today’s 8.6% CPI could very well be just the warm-up. And assuming that its components are more services-oriented, it may prove more stubborn than the 1970s breakout.

On the other hand, Powell’s rate hikes will likely be much more “effective” than Burns’s—if for no other reason than the changes to how we calculate shelter inflation. At the very least, higher mortgage rates won’t cancel out the disinflationary tightening effects.

Besides, the world has racked up much more debt since then, which makes the economy more sensitive to the cost of money. For example, corporate debt in the U.S. as a percentage of GDP is double what it was in the 1970s.

So, Powell may not have to resort to Volcker’s shocking double-digit rates to tame headline CPI growth.

But at the end of the day, does headline CPI matter at all?

Or, is it just a convenient yardstick for the media and politicians to spin bite-sized narratives because their audience can’t digest more than 300 words before zoning out into their Instagram feed?

Apart from political pressure, CPI shouldn’t affect the Fed’s policy much because it’s supposed to look at PCE as its inflation gauge. But the fact that central bankers ignore headline CPI doesn’t necessarily mean that everyone does too.

In fact, it’s an important input that adjusts prices and wages in many parts of the economy

From WEF:

The BLS recently reported that over 2 million workers were covered by collective bargaining agreements which tied their wages to the CPI. The CPI index also affects the incomes of almost 80 million people because of statutory action: 47.8 million Social Security beneficiaries, about 4.1 million military and Federal Civil Service retirees and survivors, and about 22.4 million food stamp recipients. The CPI is also used as an input for myriad other contracts in the US that will touch nearly every American household.

So, even if CPI doesn’t reflect real inflation or guide monetary policy, its growth can set off a self-fulfilling prophecy that does. And considering the parallels, this prophecy could be much grimmer than that of the 1970s.