"A Reset of Investor Expectations"—Is the Worst Behind Us?

JPMorgan says bad news is already priced into beaten-down valuations

Good morning MIMs,

Before we get into this week’s issue, let’s take a moment to remember that dollar cost averaging is the most powerful wealth creation tool that works 100% of the time (in the long run, of course).

It’s so effective that, since 1980, it has even beaten the glorified “buy the dip”:

📖 Recommended read: “buy the dip” vs dollar cost averaging analysis from Of Dollars And Data

🚀 Digital Assets

Crypto Prices Are Out of Touch with On-Chain Activity

Although crypto prices have been in an uptrend for a month now, crypto intelligence company Glassnode warns that on-chain activity still remains lackluster. This divergence raises the question: is this the beginning of a bull market or a “dead cat bounce”?

🔍 Zooming out

In the most recent report, Glassnode highlighted three on-chain statistics, which point to dwindling blockchain activity:

The number of active bitcoin addresses keeps slumping from the peak it reached last October. “With exception of a few activity spikes higher during major capitulation events, the current network activity suggests that there remains little influx of new demand as yet.

Bitcoin’s transaction volume and total fees are still within a “bear market” range. For reference, transactions are down ~40% from their Jan 21 peak and fees barely reach 14 bitcoins per day while last year they were ranging from 50 to 200+ bitcoins per day. “Whilst we have not seen a notable uptick in fees yet, keeping an eye on this metric is likely to be a signal of recovery,” Glassnode wrote.

Ethereum manifests similar symptoms. While its price has gone up over 50% within the past month, its on-chain activity remains rather lackluster. Ether’s transaction volume has been in decline since last May and its fees (aka gas prices) are at “multi-year lows.”

🔮 Looking ahead

What could launch crypto into another structural bull market?

Glassnode’s on-chain analysts suggest that an inflection point could be the capitulation of long-term crypto holders (aka HODLers), which are more sensitive to crypto prices than newcomers.

As Glassnode wrote: “Bottom formation is often accompanied by [long-term holders] shouldering an increasingly large proportion of the unrealized loss,” the report stated. “In other words, for a bear market to reach an ultimate floor, the share of coins held at a loss should transfer primarily to those who are the least sensitive to price, and with the highest conviction.”

The much-awaited crypto redistribution may be near.

Glassnode spotted first signs of HODLer capitulation in June. In a July note, its analysts wrote: “The $20K region has attracted a large cluster of Short-Term Holder coin volume. This is a result of a significant transfer of ownership from capitulating sellers, to new and more optimistic buyers.”

📈 Stocks

“A Reset of Investor Expectations” After Valuations Get the Sharpest Haircut in 30 years

This year, the stock market had its worst first-half in 50 years. The S&P 500—the key benchmark for US stocks— dropped 24%, and the tech-heavy Nasdaq shed 33% of its value.

The drop in prices, however, had little to do with company finances. (Case in point, as the S&P 500 cratered in Q1 2020, its earnings grew 4.4% compared to a year ago). Instead, it was a result of a market phenomenon called “multiple compression”.

In a "human" language, it is a reduction in the price investors are willing to pay for a dollar in a company’s earnings.

📖 Recommended read: Investopedia’s primer on multiple compression

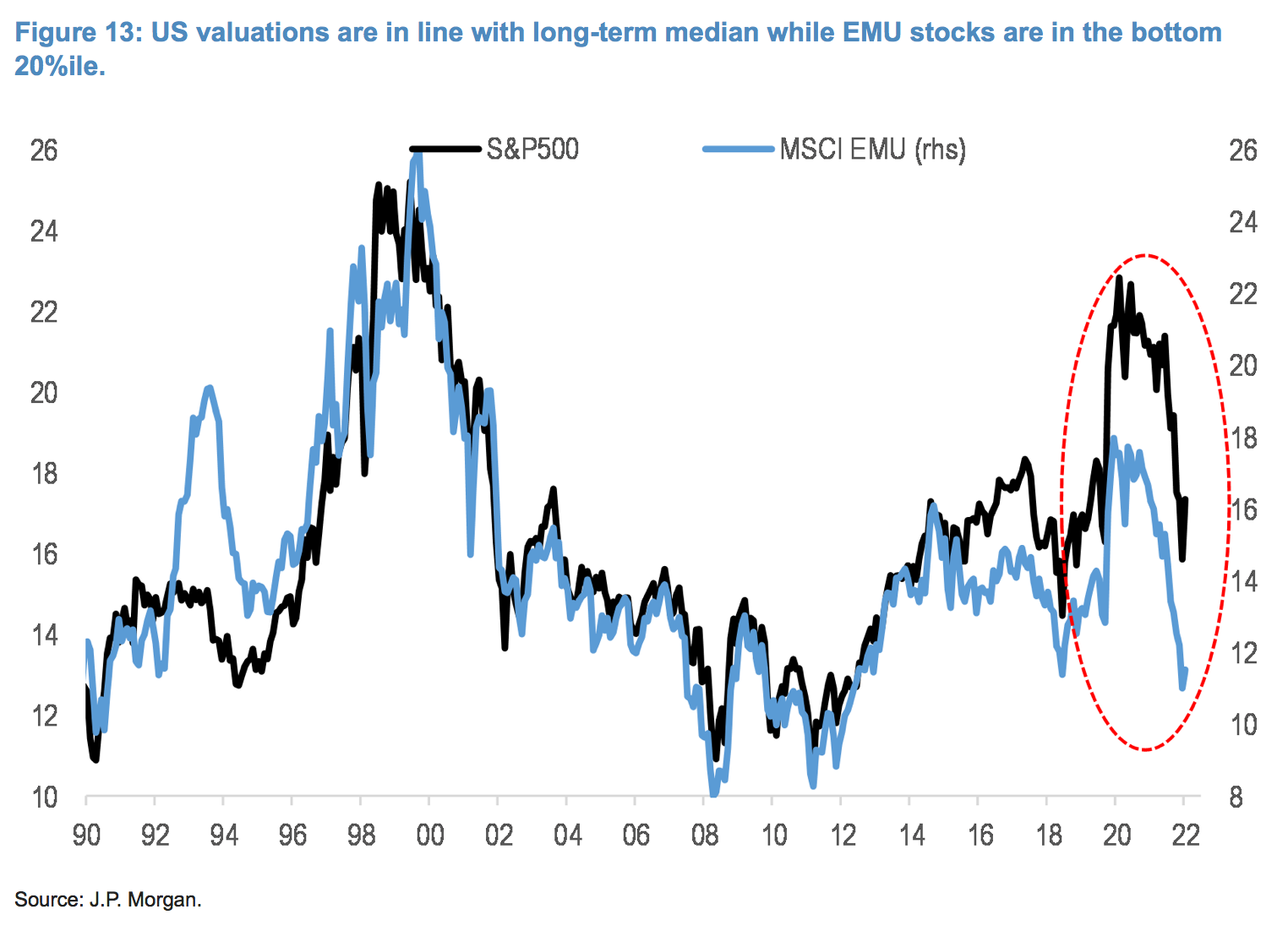

By JPMorgan’s calculations, the first half of 2020 saw the most savage compression in the past 30 years—beating the dot-com crash and the aftermath of the 2008 housing collapse.

“The S&P 500 has seen its second sharpest P/E de-rating of the past 30Y, exceeding the typical compression seen during prior recessions. While the current equity multiple is in-line with the historical median, we believe it is better than fairly valued…” JPMorgan wrote in an internal note.

🖼️ The big picture

If not earnings, what made investors have second thoughts on how much they want to pay for stocks?

Two things: 1) the Fed’s battle with inflation and the Russia-Ukraine conflict.

Since the beginning of this year, the Fed has been doling out the most aggressive rate hikes in decades to tame near double-digit inflation. Such a hawkish Fed doesn’t fare well for risk assets because higher rates increase the cost of borrowing and trim valuations.

📖Recommended read: Dan’s Forbes column on how rates affect stock valuation and why

Meanwhile, the West’s face-off with Russia over Ukraine is throwing a wrench in global supply chains of energy and food while fostering the very inflation central banks are trying to put out.

🔮 Looking ahead

The good news is that the doom and gloom priced in beaten-down valuations may be already behind us.

In the last FOMC meeting, Powell gave off a dovish undertone, hinting at a slowdown in rate hikes. Meanwhile, inflation is showing signs of peaking—all of which can bring what JPMorgan calls “a reset of investor expectations.”

“Whether it’s earnings or the Fed, we see a reset of investor expectations: Last week’s more dovish Fed meeting that saw the base rate raised close to neutral, along with softening inflation expectations and declining bond yields, indicate peak hawkishness is likely behind. Risk markets are rallying despite some disappointing data releases, indicating bad news was already anticipated/priced in,” JPMorgan analysts wrote in an internal note.

In fact, according to JPMorgan's survey, 58% of its institutional clients plan to increase equity exposure.

🏛️ Macro

Risk Assets Shrug Off Pelosi’s "Provocative" Taiwan Visit

The rumors came true.

In an unofficial detour, House Speaker Nancy Pelosi’s plane swooped down in Taiwan late Tuesday. Yesterday, she met up with President Tsai Ing-wen to vow support for the island facing growing military threats from China.

Pelosi’s landmark democratic gesture is ruffling Chinese feathers. China’s Foreign Minister Wang Yi called it “a complete farce” and threatened “targeted military actions.”

🔍 Zooming out

Nancy Pelosi is a lifelong democracy advocate and a harsh critic of China’s autocratic regime. In 1991, she made a splash raising up a memorial poster on Tiananmen Square in Beijing where China’s rulers massacred hundreds of peaceful protesters.

Pelosi’s visit to Taiwan at a time when China is threatening to take this de facto sovereign island by force is a fat slap in Xi Jinping’s face. In fact, she is the highest-ranking official to visit Taiwan in 25 years.

In response, the Chinese Foreign Ministry called the visit “provocative” and warned the US that China will take “resolute and strong measures.” So far, China has halted trade with Taiwan and launched four-day military drills aimed at the island.

🤷♂️ Why it matters

Rhetorical muscle flexing aside, it’s not yet clear what China’s ultimate response will be. Meanwhile, the markets are shrugging it all off as a trivial quarrel. The S&P 500 is up 1.5% since Tuesday.

🔦 Other macro highlights

JPMorgan expects Europe to tip into recession in the second half of 2022 due to exploding energy prices, weakening business confidence, and potential gas rationing in the coming winter

The UK is in for stagflation. The Office for Budget Responsibility (OBR ) warned that households will see the largest drop in real incomes since 1956 through the rest of 2022

In the last FOMC meeting, the Fed’s chair Powell implied that it may be appropriate to slow the pace of rate hikes. Now all eyes are on July’s job report that’s coming out Friday, which may hint at where rates are headed next.

The US is in a “technical” recession with real GDP growth slowing for two consecutive quarters. That doesn’t scare JPMorgan’s strategists who think a “mild recession” is already priced in stocks, and the worst of the bear market is behind us.

💬 CIO Quote of the Week

“Global equities managed to stage a surprising rebound in July even as central banks aggressively hiked rates, inflation continued to soar, and the war in Ukraine shows no signs of abating. However, we think it’s still too early to get excited about the July recovery given the uncertainties and headwinds ahead.”

– Mark Haefele, Chief Investment Officer, UBS Global Wealth Management

Thanks for reading Meanwhile in Markets... Subscribe and get our weekly market commentary in your inbox every Thursday!